What is a Guaranteed Investment Contract?

As it is defined in the name, it is the contract or agreement where an investor puts a specified amount of money into an insurance company for certain time period. In return, the insurance company would guarantee the principal along with a predefined return rate. Such contracts are found in pension plans and stable value funds to prevent fluctuations in returns while exposing the funds to lower risks. Such GICs in retirement plans are favorable since they are not exposed to a greater loss with the alteration of market forces.

Key Features of GICs Principal Protection:

- There is a minimum risk to loss on investment as the principal amount is guaranteed.

- GICs are therefore most appealing to conservative investors as they managed expectations of security instead of returns.

Fixed or Floating Returns:

- Investors can expect in hand few rates of returns which could either be an index or a fixed.

Defined Maturity Period:

- Additionally, there are predictable time frames to GICs as they are usually contracted for a specific period that ranges from a couple of months to several years.

In case of Issuer Stability:

- The economic resources required for the agreement is funded the insurance company issuing the guarantee, hence the requirement of creditworthiness is essential.

Types of Guaranteed Investment Contracts:

Traditional GICs

Such contracts are supported by the general fund of the insurance company, and they earn a designated interest for the duration of the agreement. They are highly utilized in defined contribution pension plans, like the 401(k).

Synthetic GICs

- Wrapped GICs are also called synthetic GICs and there is involvement a collection of stable income securities of the investor.

- The portfolio meets any shortfall in value through the direction of insurance that meets the requirement.

Immediate vs. Deferred GICs

- Immediate GICs commence accruing interest immediately after the investment is made and this is done while the other issues waiting for maturity.

- Deferred GICs have interest to be earned and which only gets paid at the conclusion of the contract.

Cashable vs. Non-Cashable GICs

- Cashable GICs has minimum features that fines accompany early withdrawal of the GIC the funds.

- Non-Cashable GIC or locked in GIC has its funds locked up until maturity and are deemed less risky because they offer more return.

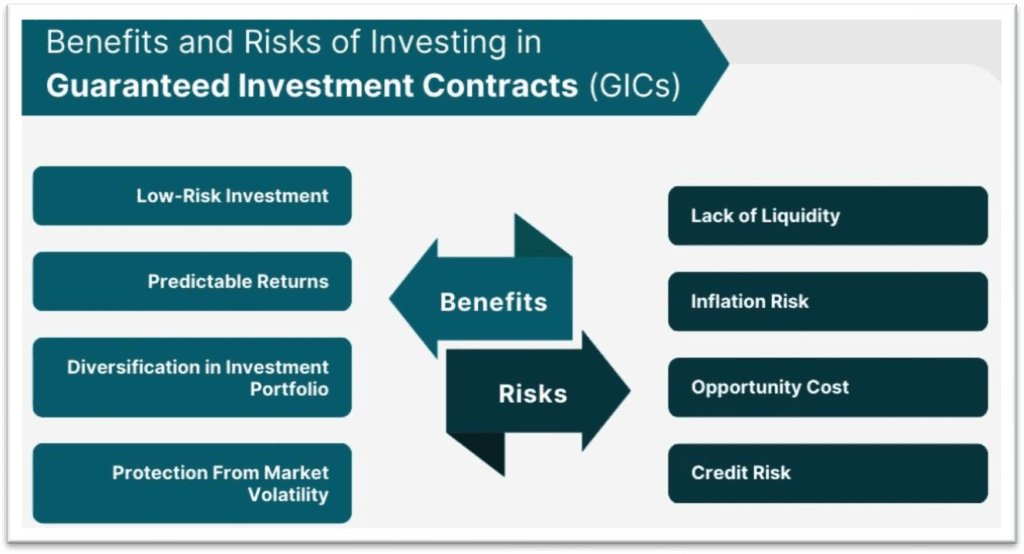

Benefits of GICs

Capital Preservation: GICs whether used for purchase of commercial property or in treasury products or for life insurance, it never goes away and keeps performing producing it a good asset for retirement planning. Final get GIC fixed returns that help establish income planning.

Predictable Income:

- Being employed and earning a rated interest guarantees a line of revenue for financial future planning.

Low Risk:

- As GICs bear a little correlation to the variations of the market, they are ideally suited for investors with deep aversion to risk of any kind.

Flexibility in Term Lengths:

- The investors get an opportunity to choose a short, medium or a extended agreement in accordance with their financial needs.

Risks Associated with GICs

1. Interest Rate Risk

In rising interest rate environments, GICs will generally offer lower returns compared to alternative investments like U.S. Treasury Securities. This is because new investments with increased interest rates become more attractive and, therefore, reduce the relative attractiveness of existing GICs.

2. Inflation Risk

The stable nature of GIC returns might not keep up with inflation over time, gradually reducing purchasing power. Investors needing an inflation-indexed alternative should consider this fact.

3. Credit Risk

The contract guarantee is only as good as the fiscal reliability of the issuing insurer. Therefore, one needs to research the credit score of a company before investing in its GICs.

Comparing GICs with Other Low-Risk Investments

Bonds are a debt security released by firms or governments. They pay regular interest and reimburse the capital at expiration. Though both GICs and bonds are based on stable earnings, they have a few differences between them as follows:

GICs vs. Bonds: The Disparities Explained

Bonds and GICs can be said to share a commonality in the sense that they both offer steady revenue, however there are a variety of differing features that these instruments have. This is because GICs are more manageable and have a limited tenor.

Credit risk: Credit rating allocated to the issuer has a significant impact on the credit profile of the bond which means earnings off the bond are quite volatile. GICs on the other hand, are regarded more reliable largely since they are traditionally backed by banks/insurance companies.

Liquidity: One key difference between the two is liquidity, instruments such as GICs are usually less liquid since they cannot be traded at a secondary market. Hence, the financial markets are typically more liquid than GICs.

Interest rate risk: Bonds are marketable and their premiums are responsive to fluctuations in the borrowing cost, such changes may in turn, affect the market value but that is not applicable in the case of GICs until the maturity of the instrument.

GICs vs. CD

There is a difference between a GIC and a CD, how each individual is approached largely depends on the level of security the person would prefer. This is because both have a fixed tenor, but a CD would offer higher returns due to how it is issued at a set rate by certain banks.

Issuers: American Banks issue the CD while GICs are issued by Canadian Banks, although the modes of GICs allow for a larger market share to be targeted. This is largely due to how Canadian insurance companies have more GICs than banks that offer them.

FDIC Insurance: However, an American GIC would have a more favorable risk adjustment ratio than American CDs since GICs are coming from Canadian banks that provide insurance against them.

Early Withdrawal Penalization: Most CDs early redemption capacity is generally less or more restrictive therefore some form of penalty may still apply.

Tips for Choosing the Right GIC Set Clear Objectives:

- Settle whether you need cash in the short-run or the cash flow’s stability at all times.

Evaluate the Institution:

- Determine the level of the insurance company’s credit risk as to reduce a risk of default.

Search for the Highest Interest Rate:

- Shop around for interest rates and choose the best options to maximize the returns.

Examine the Policy Document:

- Make certain that you know the consequences of cashing out of any GIC that has no cash surrender value before the term expires.

Real-Life Example

Let’s say Jane is an investor that is an approaching retiree. We invest in a five-year conventional GICs with an annual interest rate of 3%. Such an agreement will secure funds and provide a regular stream of rental income after retirement.

Conclusion: Secure Your Financial Future with GICs

Guaranteed investment contracts have the best of both worlds – They are secure and predictable. This serves as a basic requirement layer for investors who are ready to take some risks. GICs are beneficial either for pension planning or as part of an investment mix because they ensure the protection of the capital and retraction at all times. Being Prudent – Attending superior investment level than in other auction houses This tends to make them quite attractive to many people.

For individuals who stand to consider this investment consideration, it is prudent that the issuer’s strength be first since the terms are understood and that the investment is in sync with their personal financial goals. If you’re ready to take advantage of the GICs, speak to a financial expert to craft an approach that is right for you.

")